Image via Wikipedia

This is a guest post by Mathieu Bouville, PhD

What on Earth is the CAPE?

The price-earnings ratio (P/E) is a common tool for valuing a stock or a group of stock (such as an index). A difficulty is that there are multiple choices for the earnings. One generally uses forecasts, but these are basically guesses. One can instead prefer earnings for the past year. In any case, either of these two earnings may be negative in a recession, making the P/E ratio negative as well. And if earnings drop temporarily due to the state of the economy and the stock price drops to the same extent, the P/E ratio does not change; yet it is a good time to buy because earnings will recover along with the economy. So the P/E ratio is not a very reliable guide to time the market.

A third choice is to use a longer-term historical number, for instance the average earnings over the past ten years. The idea is that such a number gives a reasonable idea of what the earnings will be over an economic cycle. The so-called cyclically-adjusted P/E (CAPE) is simply a P/E ratio calculated using such an average over an economic cycle for earnings.

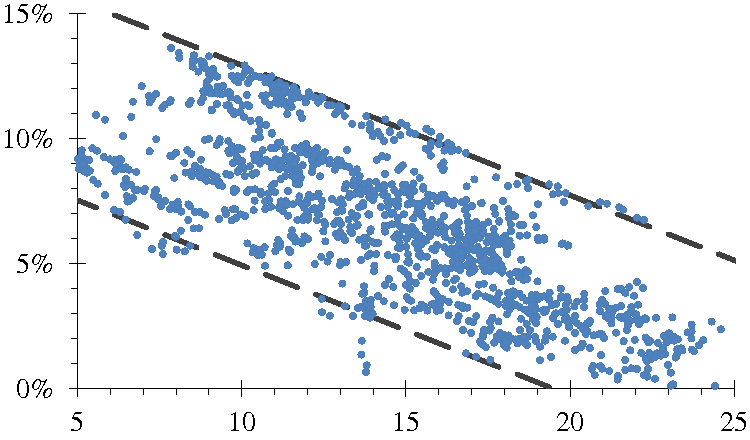

The historical average of the S&P 500 CAPE was 16.4 (and the median was 15.8). When the CAPE is quite above this value, stocks are deemed expensive, and cheap when the CAPE is low. The CAPE was at or above 30 for three months in 1929, and we all know what followed. It was even above 40 in 1999 and 2000!

The predictive power of the CAPE

Figure 1 shows the annualized real return over the next 20 years as a function of the current CAPE. When the CAPE was below 10, the return of the S&P 500 has never been below 5% p.a. over the next 20 years (i.e. one at least multiplied one’s purchasing power by 2.7). And it has never been above 3% when the CAPE was above 23. (This does not mean that this will never happen, just that it is quite unlikely.) With the 1999–2000 CAPE of more than 40, it is hard to see how one could dream of making money in the long run.

The S&P 500 CAPE is currently around 20. We can thus expect a real return over the next twenty years of somewhere between 0 and 7.5%. This implies that it is unlikely that the return will match the historical average of 6.5% p.a. Note that other markets (for instance in Europe) can currently have lower values of the CAPE.

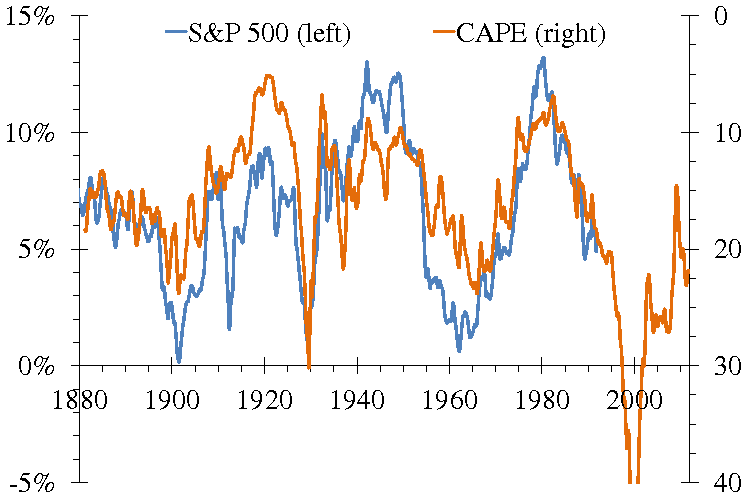

The blue line in Fig. 2 shows the annualized real return over 20 years for the S&P 500 (known up to August 1991). The orange line corresponds to the CAPE (the scale is inverted, so the curve going up means that the CAPE decreases). The CAPE is reasonably well correlated with the real return over the next twenty years.

The main failure is seen in 1912: the CAPE did not stand a chance of predicting what would happen twenty years later in 1932. Likewise the CAPE was overly optimistic between 1955 and 1965, but what it missed was the high inflation of the seventies. The return over the coming twenty years depends on how expensive the market currently is and on what may happen in the next two decades, but obviously the CAPE can know nothing of the latter.

If the CAPE has some predictive power, it can be used to improve the efficiency of one’s asset allocation. One can for instance increase one’s equity allocation when the CAPE goes down, since future returns should improve. The CAPE going down means that the price is going down, so instead of just rebalancing one would increase the target allocation. For a stock–bond allocation of 50–50, if the stock market loses 20% one is now at 40–50. Rebalancing means selling 5 units of bonds and buying stocks to get to 45–45. But since the CAPE is now lower one could instead wish to aim for something like 50–40, i.e. over-rebalancing.

Strategy based on the CAPE

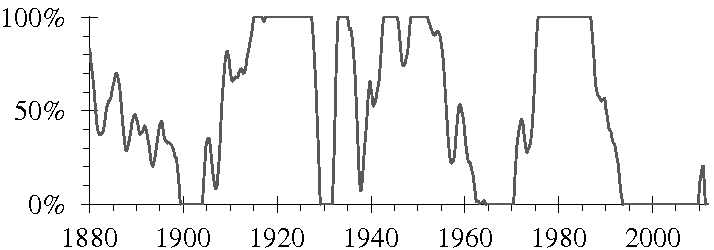

Historically, the CAPE was between 11.6 and 19.7 half the time. We will consider this range as normal: anything lower (bottom quartile) is cheap, and anything higher (top quartile) is expensive. At or below 11.6 we will hold 100% of stocks, but only bonds if the CAPE skyrockets to 19.7 or above. The stock allocation will vary linearly between 11.6 and 19.7, as shown in Fig. 3. If CAPE = 16 then one holds 46% in stocks for instance. I will use the S&P 500 for the stock allocation and 10-year U.S. treasuries for bonds (mostly because data are easily accessible at http://www.econ.yale.edu/~shiller/data/ie_data.xls).

The stock allocation cannot depend on the CAPE in this simple way: if the CAPE goes from 10 to 25 and back down to 10, you would sell at 20 and then buy back at 20. This way, you may reduce volatility somewhat but you would make no extra money. It would be better to sell at 22 and buy back at 18.

Instead of the current CAPE value, we use the average over the past two years. This creates a delay in buying and selling: you do not sell as soon as stocks get expensive, i.e. you do not exit the market far too early (when prices are still increasing). Likewise you do not buy as soon as prices are low (but still going down). This adds an implicit element of momentum: a CAPE of 20 when markets go up is treated differently from a CAPE of 20 when markets go down. The blue line in Fig. 4 shows that the result is indeed good. (Another advantage is that it changes more smoothly, so one does not have to buy lots of stocks now to sell them back in a month, as shown by the bottom plot in Fig. 4.)

The equity allocation dropped to zero from early 1929 to the end of 1931 to jump to 100% in 1932 (staying there for several years). This feature is what makes the CAPE strategy superior to static stock–bond portfolios: you dump stocks as they get overpriced and buy them back at bargain prices. You thereby dodge the bursting bubbles exhibited by the black line in Fig. 4.

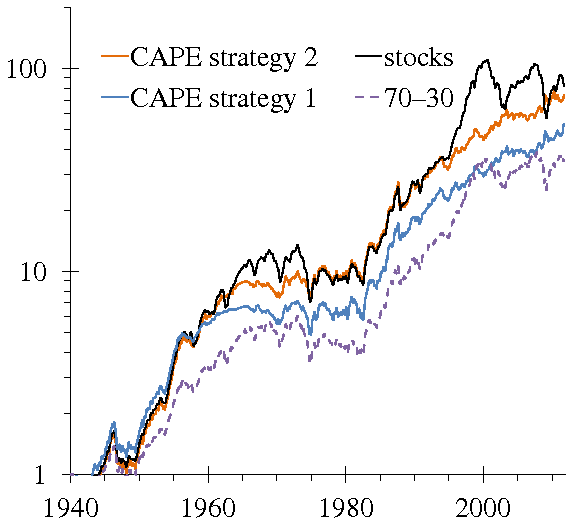

Consequently, the CAPE-informed strategy can return about as much as stocks, but with lower volatility (14% against 19%), and with much smaller drawdowns (drops from peak to trough), as shown by Table I.

Table I: The nominal drawdowns for the S&P 500, a 70–30 portfolio and the CAPE-based strategies for several time periods.

The equity allocation is zero again from 1994 to 2008 (yes, a decade and a half). Over this period, a stock investment behaved like a roller-coaster. The CAPE-based strategy, on the other hand, grew very steadily, as shown by Fig. 5. Between 1995 and today it did about as well as stocks, but its worse drawdown was around 10% over the period (instead of a dive of more than 40% followed by another of 50% a few years later), as shown by Table I.

The blue circle in Fig. 5 shows the return of the CAPE-based strategy as a function of its volatility. It compares very favorably with static stock–bond portfolios (solid line).

Varying the strategy

The dashed line in Fig. 6 corresponds to increasing by half the outperformance compared to a 10–90 portfolio (the allocation with the lowest volatility): 1.5 × (portfolio return − 10–90 return) + 10–90 return. It so happens that by changing the thresholds in Fig. 3, one can obtain CAPE-based strategies that follow this line pretty well (an efficient frontier for these strategies). I have no idea why. In any case, this shows that the outperformance is greater for greater stock allocations (and the difference is of course even larger when compounded over decades).

One may tweak the strategy a bit further and get the orange line in Fig. 6: an average 62% allocation to stocks, a return of nearly 7.9% p.a. for a volatility of 14.3%. This second strategy is shown as an orange diamond in Fig. 5.

The outperformance during the thirties is huge. After that the strategy tracked stocks, only with fewer bumps in the road (right part of Fig. 6) — just what one wants to use the CAPE for. And after 1990, it went up smoothly while the stock roller-coaster was making everyone vomit without returning much more than this strategy.

Table II shows that the biggest drawdowns ever for the two CAPE-inspired strategies (28–29%) were smaller than the sixth biggest one for stocks (34%). The second CAPE-inspired strategy outperforms the first one essentially in the early twentieth century, the thirties and the sixties; its strength is an ability to keep in stocks more at the right time, rather than a greater likelihood of avoiding losses (drawdowns are very similar).

| rank | 1st | 2nd | 3rd | 4th | 5th | 6th |

| stocks | 82% | 49% | 42% | 39% | 38% | 34% |

| 70–30 | 43% | 29% | 27% | 24% | 24% | 20% |

| CAPE strategy 1 | 28% | 24% | 23% | 19% | 19% | 17% |

| CAPE strategy 2 | 29% | 28% | 26% | 23% | 20% | 13% |

Table II: The worst nominal drawdowns from Table I for the S&P 500, a 70–30 portfolio and the CAPE-based strategies.

Over ten years, there is about a 5% probability of losing purchasing power using a CAPE-based strategy, whereas with stocks there is a 5% probability of losing about 22% in real terms. It takes 15 years for stocks to have a 95% chance of making money in real terms.

Historically, the worst result over twenty years was a gain of 24% in real terms with the CAPE-based strategy, against a loss of 22% with stocks. Since the strategy reduces the risk of a major loss compared to an investment in stocks it can be used more safely for shorter time horizons. Note, however, that the focus of this post was strategies returning about as much as stocks, not strategies designed for the short term.

A few comments

Everything presented here is based solely on dynamic changes to the stock–bond allocation. There is no short position. There is no stock-picking. There is no leverage. There are no asset classes other than stocks and bonds. The strategies use only data that are publically available (e.g. at http://www.econ.yale.edu/~shiller/data/ie_data.xls).

A drawback of these strategies is that they may require to stay out of the stock market for over a decade. And I am not sure whether one would have the nerve to try to beat stocks by shunning equity for so long. Note that it was assumed that bonds would be bought in such instances, but you may decide to look elsewhere when stocks are expensive (e.g. real estate).

It seems that a weakness of these strategies is that they buy bonds when stocks are deemed expensive, regardless of the intrinsic appeal of bonds. I tried taking bond yields into account (using a kind of equity premium), but results are similar. The most plausible reason is that when the stock market is set for a crash, what matters is simply selling stocks.

A common claim regarding any strategy is that if it were so easy to outperform, everybody would do it. But one must remember that mutual funds care about returns only indirectly. Why will they not stay out of the market for half a dozen years when there is a bubble? Because by the time they are proven right (having a higher return than competitors with lower volatility), the fund has been closed down because all “investors” fled. The main risk for fund managers is outflows, the rest matters only inasmuch as it can lead to outflows.

This guest post was written by Mathieu Bouville, PhD

I appreciate the detailed analysis that Dr. Bouville has brought to the table; thanks for the great guest post! Dear reader, what are your thoughts on the cyclically-adjusted P/E (CAPE) and how it relates to asset balancing and investing in equities?

This is one of the best blog articles I have ever read. This strategy works! I have implemented this strategy for years but never put it down on paper as well as you have here. The Arbor Asset Allocation Model Portfolio (AAAMP) uses what I call a “tactical asset allocation strategy”. My “normal” is to stay between 25% and 65% net long stocks depending on valuation. Here is my explanation of a tactical asset allocation for anyone interested:

http://ArborInvestmentPlanner.com/tactical-asset-allocation-strategy.php

I was expecting to read about Cape Cod. Haha, instead I’m hit with stock information! 🙂 Nah, great blog post. Very informative!

“I was expecting to read about Cape Cod.”

Keviiiin, there is a naughty man calling my post fishy!

Wow. Just Wow. Great analysis and explanation.

A drawback of these strategies is that they may require to stay out of the stock market for over a decade. And I am not sure whether one would have the nerve to try to beat stocks by shunning equity for so long.

This is the future of investing analysis, in my assessment. My thanks to Mathieu for writing this powerful article and to Kevin for hosting it. I would be grateful, Mathieu, if you would provide me with an e-mail address so that I can get in touch with you. I am Rob Bennett at hocusreports@verizon.net. My site is at http://arichlife.passionsaving.com . I’ve done a lot of work exploring ideas relating to what you are putting forward here and would love to discuss possibilities with you.

The concern you address in the words quoted above is a big one in the eyes of many people. My belief is that it is not a problem. To understand why, you need to understand why it is that stock prices get to the levels they have been at for the past 16 years in the first place.

All stock overvaluation is the product of investor irrationality. This is so by definition. If investors were rational, they would always price stocks properly. That is, valuations would always be at fair-market levels.

Say that we were to publicize CAPE (I call it “P/E10”) and provide tools to investors to help them make use of it in setting their stock allocations. If we did this, every tick upward in the P/E10 level would cause some sales of stocks, bringing the P/E10 level back to fair-value level. Every tick downward would bring buys, which again would bring prices back to fair-value levels. Stock market prices are naturally self-regulating! We don’t need to worry about overvaluation or undervaluation ever again.

But we have it! How can I say that we don’t need to worry about it?

We have overvaluation today only because most of today’s investors are not aware of the realities you are discussing in this article. Most people today believe in Buy-and-Hold, which is rooted in an OPPOSITE premise (that stocks are always worth buying and that returns are not predictable). The correlation that you are discussing here was discovered by Yale Economics Professor Robert Shiller in 1981. Prior to Shiller’s research, people just didn’t know about this!

We are entering a new era in our understanding of how stock investing works. There are many huge insights that were discovered during the Buy-and-Hold years (the most important is the discovery that short-term market timing doesn’t work). The next step is to incorporate Shiller’s insights into the Buy-and-Hold Model to produce something entirely new (I call the something new “Valuation-Informed Indexing”). The numbers show that, when we do that, we will be able to reduce the risk of stock investing by close to 80 percent. We are headed into some very exciting times for stock investors.

The problem we have had getting these ideas publicized is that Shiller’s model is so at odds with the Buy-and-Hold Model (which is rooted in the research of University of Chicago Economics Professor Eugene Fama). People who have learned about the research of the 1960s and 1970s have a hard time accepting that the research of the 1980s forward really says what it says.

Fama’s research can be reconciled with Shiller’s research. I’ll hold back from saying how in this post, but, if you ask, I am happy to go into that. The hurdle we face today is in getting people who have for years believed in Buy-and-Hold to understand that the research on which that model was based was tentative research and that we have learned more in recent decades and that we now need to incorporate the new findings into the mix to come up with something 10 times more powerful than anything that has been possessed by any investors of the past.

Super article!

Rob

“The problem we have had getting these ideas publicized is that Shiller’s model is so at odds with the Buy-and-Hold Model (which is rooted in the research of University of Chicago Economics Professor Eugene Fama)”

Buy-and-hold existed before Fama was even born.

I don’t believe that using the CAPE is at odds with buy-and-hold. Look at the orange line at the bottom of Fig. 6: it follows the stock line (in black) most of the time, this is just plain buy-and-hold as long as valuations are sane. This strategy is closer to buy-and-hold than to, say, day-trading or stock picking.

I’m a big fan of the CAPE style investing you posted on. “Buy-and-hold”, as it is used today, means an investment style where you permanently set your allocation regardless of valuations, world events, …. whatever. Modern-day “buy-and-holders” simply do not market time. In my opinion, that bears no comparison whatsoever to the alternative you’re proposing. Just because the CAPE method will leave allocations unchanged for long periods of time does not make it “buy-and-hold” in the sense that that term is currently used by “Bogleheads.”

“The concern you address in the words quoted above is a big one in the eyes of many people. My belief is that it is not a problem.”

I did this, so I am in a good position to know that it is a reasonable strategy. But even I am not sure that I would stay out of the market myself for over a decade. So people less convinced about the validity of the strategy would be even more skeptical.

Note however that the second model (orange line) has a higher turnover than the first (blue line), so it would not stay out of the market as much (but still quite a bit in the past 20 years).

Look at the orange line at the bottom of Fig. 6: it follows the stock line (in black) most of the time, this is just plain buy-and-hold as long as valuations are sane. This strategy is closer to buy-and-hold than to, say, day-trading or stock picking.

I certainly agree that the strategy you suggest (I call it “Valuation-Informed Indexing”) is closer to Buy-and-Hold than it is to day trading or stock picking. I would describe it as a revision to Buy-and-Hold, based on Shiller’s research, which was published several years after the publication of A Random Walk Down Wall Street, the book that Buy-and-Holders cite as their Bible.

There’s only one difference between VII and Buy-and-Hold — Valuation-Informed Indexers make infrequent adjustments to their stock allocation percentages. But that one difference makes a huge difference to the long-term results obtained. VII produces far higher returns at greatly diminished risk. More importantly, it makes the investing project far less stressful. Buy-and-Holders never know what is coming. VIIers always know what’s coming (not precisely, but close enough). That’s huge.

Another huge difference is that Buy-and-Hold causes economic crises that we could avoid if we publicized VII. Since 1900, there have been four times when we have gone to P/E10 values above 25. There have also been four economic crises in that time. Each and every one of them followed the time we hit 25 by a few years. Why? The return to fair value P/E10 levels take a huge amount of spending power out of the economy, causing an economic crisis. The market was overpriced by $12 trillion in 2000. Today’s crisis became inevitable when we let prices rise to the insane levels to which we permitted them to rise in the late 1990s.

Buy-and-hold existed before Fama was even born

There’s a sense in which I agree with you and there is a sense in which I don’t, Mathieu.

The idea of not taking price into consideration when setting one’s stock allocation has been with us since the first market opened for business. I agree with that. I call that approach “Get Rich Quick” and I think it can be fairly said that Buy-and-Hold is just the old Get Rich Quick concept dressed up in modern, pseudo-scientific clothing.

The sense in which I would describe Buy-and-Hold as something new is that Buy-and-Hold purports to be rooted in research. Those promoting Buy-and-Hold strategies often claim that “timing never works.” There is of course precisely zero research showing this to be so. There is research showing that short-term timing never works. But every study of long-term timing shows that it always works. So the statement “timing always works” is every bit as true as the statement “timing never works.”

I think it would be fair to describe Buy-and-Hold as a marketing gimmick. Millions of middle-class investors have been led to believe that long-term timing is not required. They believe that there is some study somewhere showing this. So, when their common sense tells them that they had better lower their stock allocations because prices have risen so high, they ignore that voice on grounds that all the experts say that timing isn’t required. But of course there is no research supporting such a claim. It’s just a means by which stock salesmen persuade people to buy stocks even in circumstances in which stocks offer a poor long-term value proposition.

Rob

So at current CAPE you should be holding more fixed-income products than equities? CAPE looks great in the rear view during periods of decent real yields on fixed-income, but how long are you going to hold fixed income products with current yields?

What kind of average maturity should you seek using the above model? That’s even more important than allocation; do you buy the long bond? Keep maturities at 6-7 year averages?

I’d like to hear an answer. Let’s forward test this model. 😉

The best reason to buy bonds and/or other debt instruments is for capital preservation, not yield. Yield is just a nice bonus that sometimes comes along with your relatively safe capital preservation investment.

So what happens when the yields are lower, you ask? I guess someone that actually cares about the yield as a critical component of these investments would need to answer you.

Or let me rephrase my position. I think of it as the author of the article does. I’m not so much invested in bonds and/or other debt instruments as I am either in or out of the stock market. You have to put your money somewhere. If I’m afraid of a sudden and fast rise in interest rates, I’ll just use short-term bonds – again, not for yield, but just to ensure that my capital is preserved, for the most part.

Let’s forward test this model.

The proper person to respond to your other questions is Mathieu, the author of the article. But I wanted to address this one point just so that people don’t get a wrong idea about what this is all about, JT.

Forward testing is certainly a good idea. It’s very hard to forward test this concept, however, as it takes 10 years for the correlation between valuations and stock returns to become statistically significant.

There was a brief paper or note written once by Brad DeLong in which he made the point that it has been possible to forward test Shiller’s 1981 research (which started the ball rolling on this concept) for 30 years now. DeLong said that the doubts that were justified in 1981 (because Shiller’s findings are the result of backtesting rather than forward testing) have to a significant extent been overcome because Shiller’s theory has continued to prevail over Fama’s theory for the 30 years since Shiller published his findings.

Another way to forward test Shiller would be to look at what he said in his Federal Reserve testimony in 1996 and then consider where things stand today. Shiller said that valuations were so high in 1996 that those highly invested in stocks would come to regret it within 10 years or so. The crash came in 2008. My view is that that is close enough.

Shiller also predicted the economic crisis (caused primarily by Reversion to the Mean of stock prices) in his book Irrational Exuberance, published in March 2000. He said: “The real losses could be comparable to the total destruction of all the schools in the country, or all the farms in the country, or possibly even all the homes in the country.”

All that said, predictions based on P/E10 made today cannot be verified or discredited until 2021. It takes 10 years for the correlation between valuations and stock returns to become statistically significant. Shorter term predictions DO NOT WORK.

The reason is that it is investor emotion that determines stock returns in the short run and it can take as long as 10 years for investor psychology to turn. The Shiller model (I call it “Valuation-Informed Indexing”) says that long-term returns are caused by economic realities and thus always highly predictable (and thus long-term timing always works) but that short-term returns are caused by investor emotions and thus never predictable (and that short-term timing thus never works).

Rob

I understand that market timing works; and I think there’s plenty of legitimacy to this model. I think most any value-oriented investor uses it, at least a derivative of it, because it really is just a 10-year earnings yield calculation. Earnings yields aren’t breakthrough by any means, and they do provide for a lot of insight about long-run returns.

That said, it’s unfortunate that this model invests so much time into looking at the past 10-years earnings relative to current valuations (basically an earnings yield) but does nothing with interest rates. It’s like it went all out to calculate the theoretical returns from earnings, but never at all bothered to compare them to the available yields in the debt markets.

There’s a lot more to investing than buying/selling based on earnings yields. The Schiller, or VII approach, whatever you want to call it, provides nothing on the debt yields side of the equation. It’s one thing for equities to be overvalued based on historic earnings; it’s another to be overvalued compared to record low yields in fixed-income. Current CAPE is around 20, according to the article, which is essentially 5% a year if you smooth it. 10-year, AAA-rated corporate bonds yield little over half that, or 2.7%.

I’m not sure if CAPE was designed to effectively ignore the value of cash on the balance sheet, either. It does, but is it by design?

I think it’s an interesting strategy. I think it takes the sophistication up a level from “buy and hold,” but still half-asses it in terms of making decisions based on broad asset allocation. Over-valued or undervalued, there are always firms worth owning that sell for less than their PE10 valuation. Presuming they’re firms that are attractive in a buyout, why not take the system a step further and buy good names when the PE10 value warrants a purchase. You’ll always get the full discounted cash flow (even better, actually) in a buyout.

One step forward, but one step back. Makes sense, as any earnings yield calculation should, but it’s still lacking, in my view. I’d love for a VVII/PE10 fan to say with certainty the EXACT average maturity that is supposed to be found in the bond allocation, as this would provide far more clarity.

JT, I’ll do my best to respond to your question. In general (and especially in this example) the main benefit for being in bonds is that you are NOT in equities. If you are unsure what maturity to have, you can just go with the broad market vmbfx – If you are concerned about interest rates, go with short term vbisx.

A good alternative is to go with TIPS since in the times of greatest uncertainty, those seem to be oppositely correlated with equity. Maybe go with a 50/50 between the total bond market and TIPS. Just have a well thought out plan, and stick with it.

I personally do use the CAPE in determining my asset allocation. my allocation curve has a very similar similar shape to the one in Figure 3 above, though has more of a curve to it so I don’t get to zero until a CAPE of 25. Again, stick with a well thought out plan. Confidence in your plan is crucial when you see the market dropping – and especially when you are trailing the market (like in 1998).

Great stuff here – I’d love to see more on the topic.

Thanks Mathieu for your great analysis.

On December 3rd 1996 when Shiller made his Federal Reserve testimony the S&P500 closed at 748.28. When I checked a few moments ago it stood at 1,200.12. Buy and Hold Investors have done quite nicely.

Over-valued or undervalued, there are always firms worth owning that sell for less than their PE10 valuation.

That’s 100 percent true, JT.

There’s more than one way to make use of these findings. You are suggesting strategies that sophisticated investors might use. My particular interest is in providing super-simple strategies for the millions of typical investors who don’t want to do research. For that group, this is a HUGE step up from Buy-and-Hold. It greatly increases returns while dramatically reducing risk. In the typical case, it allows the investor to retire five to ten years sooner than he could following a Buy-and-Hold strategy.

Another huge advance is that, when this becomes widely known, we may be able to put economic crises of the type we are living through today permanently behind us. Every economic crisis we have seen from 1900 forward was caused primarily by high stock valuations (the crash that inevitably follows reduces spending power by trillions of dollars, causing tens of thousands of businesses to fail). If we let people know that stocks are not worth buying at certain prices, we will never see another bull market. Once prices get too high, enough people will sell to bring prices back to fair-value levels. Stock prices become self-regulating once investors are informed as to the realities. This is of course of big significance from a public policy standpoint.

I agree, though, that there are lots of other uses to which this could be put. I am confident that there are scores of things that no one has even talked about yet, but that will be discovered in time.

Rob

“For that group, this is a HUGE step up from Buy-and-Hold.”

Absolutely agree; and the cost-to-benefit in terms of time to returns is easily justified.

On December 3rd 1996 when Shiller made his Federal Reserve testimony the S&P500 closed at 748.28. When I checked a few moments ago it stood at 1,200.12.

Fair enough, Evidence. Thanks for providing the numbers.

Is that good enough? That’s my question to you.

If you believe in Buy-and-Hold, you believe it is good enough. Why? Because you believe that stock market prices just reflect economic realities. So it is what it is. You are getting what the economic activity says you should get, and that’s obviously the best you can hope to get, so there’s nothing to complain about.

I ask that you please try to understand how things look to someone seeing it from a different perspective. Valuation-Informed Indexers believe that the U.S. economy is sufficiently productive to generate an annual stock return of 6.5 percent real. During bull markets, we borrow gains from our future selves to temporarily pump up the S&P numbers. Then we see lower returns from that point forward until we have paid back the debt we incurred.

At the end of 30 years, it all comes out even. Buy-and-Holders and Valuation-Informed Indexers agree that at the end of 30 years the return is likely to be something in the neighborhood of 6.5 percent real. So does it matter?

I think it matters a great deal. Because we borrowed $12 trillion of wealth from our future selves to finance the bull market of the late 1990s, we are now living through the second worst economic crisis in U.S. history. Is that a good thing? And millions of us planned our financial futures in the late 1990s on the presumption that we would see returns from 1996 through 2011 higher than the ones you are showing with those numbers (and much higher than what we will be seeing in future days, in the event that Shiller’s research is legitimate). And so we spent more than we otherwise would have spent. And we handed in resignations that we couldn’t afford to hand in because the numbers we were using showed that we were ready for early retirement when in fact we were not.

Buy-and-Hold performs well at times because stocks are such a wonderful asset class that any strategy that causes you to invest heavily in stocks is going to perform well at times. But stocks have not performed as well from 1996 forward as they would have had prices not been as high in 1996 as they were. That’s my belief. Stocks can perform only as well as what the economiv realities justify and when we push prices up to phony, unrealistic levels for a time, we cause future returns to be lower than they would otherwise be and thereby do great harm to our future selves and indeed to our entire free-market economic system.

That’s my belief anyway, Evidence. I could be wrong. Lots of good and smart people believe strongly that I am. I am grateful to you for taking time out of your day to present the other side of the story with a factual and fair and informative and helpful post.

Rob