The following is a guest post by Mathieu Bouville.

Drawing an income changes everything

The usual viewpoint of investment advice is that of someone twenty or thirty years away from retirement who wants to accumulate a capital for retirement. Here I instead focus on somebody who is retired and wants an income. This case is more different than one may believe. One may think that if money is invested in stocks yielding on average 7% p.a. in real terms (i.e. adjusted for inflation) then it should be possible to withdraw every year 7% of the initial capital (increased for inflation) and last forever (at least financially).

The dashed lines in Fig. 1 show that if one leaves money invested, the market going up then down or down then up makes no difference: all that matters is the long-term average growth rate, not the path. But if one draws a constant income (equal to the long-term rate of return), whether the market first goes up or first goes down makes a big difference. Of course if the market increases regularly (black lines) then drawing an income equal to the market return (e.g. equal to the interest after inflation of a savings account) leaves the initial capital untouched. But things are different with volatile markets. After the market goes down the capital is hit (by the market fall and the income) and the subsequent market rally is not sufficient to make the capital grow again, as the solid red line shows. (If the market first goes up then down, solid green line, the final amount is slightly higher than the initial capital, but this gain is much smaller than the loss if the markets initially fall.) With volatile investments, the income one can safely draw is lower than the average return of the portfolio.

Figure 1: Three time evolutions ending at the same value if the investment is left alone (dashed lines) but not if an income is drawn (solid lines). |

Two possible goals

I consider the case of someone who needs a regular income (increasing with inflation) and expects to live another thirty years (e.g. someone who just retired at 65 and wants to be safe until 95). Two possible goals are considered: (i) not running out of money alive and (ii) maintaining one’s capital in real terms, i.e. living off the returns only (for instance to leave money to one’s heirs).

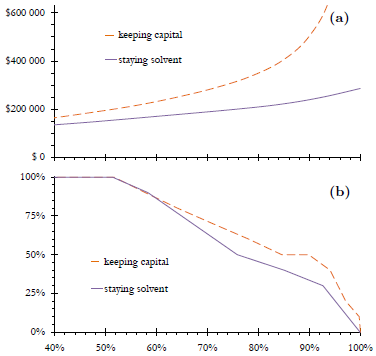

Figure 2: The probability of keeping one’s capital after inflation and of staying solvent as functions of the asset allocation when drawing $3500 (a) and $5000 (b) a year for 30 years from an initial capital of $100 000. [Enlarge figure] |

Figure 2 shows how the probabilities of keeping one’s capital and of staying solvent when drawing a regular income depend on one’s asset allocation. For an annual income of $5000 for 30 years from an initial capital of $100 000, Fig. 2(b) shows that the risk of running out of money is minimized (to slightly lower than a quarter) by a stock–bond portfolio about half in stocks. Figures 2(a) and 3(a) show that the optimal allocation may depend dramatically on one’s objective: for an income of $3500, it takes 100% cash to stay solvent but over 70% equity if one wants to preserve the principal. One needs a clear objective before choosing an asset allocation.

Figure 3: Same as Fig. 2 for a few selected asset allocations. |

How much income can be safely withdrawn

Figure 4 shows the probability of keeping one’s capital and of staying solvent as functions of the level of income that one draws. The optimal allocation is found in Fig. 2: for every income level one looks for the allocation maximizing the probability of reaching one’s goal. Of course, it is harder to keep one’s initial capital than to simply stay solvent (i.e. never lose all of one’s money): with an income of $3500 one is nearly sure to remain solvent for thirty years (with 100% cash) but an income of $2000 has only a 90% chance of keeping the principal intact (with 50% equity). The equity allocation increases with the income one wants and for incomes over 6.5% of the initial capital one will hold only equity, regardless of whether one wants to preserve principal or to stay solvent, Fig. 4(b).

The thin black line in Fig. 4(b) is the stock allocation that would produce —on average— this annual return (see http://mathieu.bouville.name/finance/investing-short_term.pdf for why this is not a single straight line). This is the allocation one would have naïvely picked to generate a given income (e.g. 70% stocks and 30% bonds for a real return of 6% a year). Clearly this is quite inadequate: what should supposedly generate the necessary income (and thus leave the capital untouched) may not even be enough to stay solvent for thirty years.

Figure 5 inverts Fig. 4 : if one wants a certain probability of keeping one’s capital (or of staying solvent) after thirty years of drawing $10 000 a year, the curve gives the capital that is needed (this is of course proportional: to get $20 000 a year, one needs twice as much). Certainty to remain solvent for thirty years requires a capital of nearly $300 000, i.e. the total amount that will be withdrawn. The needed capital drops to $250 000 for a 92% chance. To have a 90% probability of keeping one’s principal intact in real terms it is necessary to have half a million, but $200 000 are enough for a 50% chance: certainty costs money.

Figure 5: Portfolio needed for an annual income of $10 000 (a) and optimal stock allocation (b) as functions of the probability of keeping one’s capital after ination or of staying solvent. |

Methodology

These results are based on Monte Carlo simulations using normally distributed returns. The average real returns are 7% p.a. for stocks and 3.5% for bonds, standard deviations are 0.18 and 0.09 p.a. [Source: J. C. Bogle: Common Sense on Mutual Funds (Wiley, 1999)]. The correlation between them is taken to be 0.25.

In plainer English, this means that I treat the market as random in the short term but not in the long run. Similarly, with dice you do not know at all what the next roll will be but you do know that each result has a probability of 1 out of 6. Rolling dice many times (or writing a computer program to mimic these rolls), it is possible to determine the probability of certain events, such as how often you will roll 1, 2, 3, 4, 5, 6 in order. With similar computer simulations one can find out the probability of running out of money when drawing a certain income.

This guest post was written by Mathieu Bouville, PhD, who uses quantitative methods for investment optimization at http://mathieu.bouville.name/finance/. Mathieu has also recently written Investing: Four Misconceptions on Risk; thanks for the great guest posts, Mathieu!

Very interesting. I would like to see these types of studies done assuming 2 years of payments in a short-term fund ($8,000 say for the $100,000 portfolio) from which payments are taken and dividends and interest fed into. Actually it would be preferred to make it dynamic. If from day 1 market drops feed short-term fund. Otherwise reinvest dividends and interest. In this way you avoid the killer liquidations required from a big downturn in the beginning – the so-called “sequence of returns” problem you mention.

Also, be careful with “black swans”. We can calculate probabilities for dice without a simulation – not so for market returns.

Except with 100% stocks, the allocation is rebalanced annually. So when the stock market is down, you do draw your income from elsewhere (cash or bonds). I don’t explicitly distinguish between a portfolio to generate revenue and a cash account for a rainy day. Instead I ask, without preconception, what the best allocation is for a given goal: a cash allocation generally arises naturally. As I point out, if it does not it is a bad sign.

I want to quit the rat race early, but the plan is to not draw on the investment for another 25 years. Once I start drawing on the investment, I’ll reduce my stock market exposure to 20-30%.

a lot of data to process in this post.

so i am assuming the gap between the time you retire to the time you withdraw will be filled by liquid savings (cash/CDs)?

Great article! I agree that people should be focusing on income during retirement rather than a huge nestegg; especially if that nest egg is sitting in the stock market. That gets incredibly risky! Passive income is the way to go.

Although I expect to increase the income side of my portfolio when I retire, I expect to live 25 years in retirement. So I would use a combination of income and growth.

Good post! I have been telling people this kind of information for years! It is nice to see it all backed up and proven by the numbers. Like DIY above I would be interested in seeing these same numbers from the beginning of a retirement with 2 years worth of cash left out of the numbers. It is very prudent to have a cash account and use it when the market is down especially. The numbers never lie but there are so many different scenarios that could radically change the results that the possibilities are endless.

Thanks again! I will refer my engineer and other numbers clients over to check out your post!

Keith

great and timely article for me as i was having the same discussion with my dad earlier in the week. there is always a risk of earning money the hard way and then leaving it for the government custodians to keep it (fed, taxes, etc). i like the proposed methodology discussed.